DISCLAIMER — Not financial advice. Educational content only, not an offer or solicitation to buy or sell any security. Biotech and small/mid-cap stocks are highly speculative and volatile and can result in a partial or total loss of capital. Do your own research and consult a licensed advisor where appropriate. / Contenuti a solo scopo informativo e didattico, non costituiscono consulenza finanziaria né offerta o sollecitazione al pubblico risparmio ai sensi delle normative CONSOB e SEC. Le azioni biotech e le small/mid cap sono strumenti altamente speculativi e volatili e possono comportare la perdita parziale o totale del capitale investito. Si raccomanda di effettuare sempre le proprie ricerche e, se necessario, di rivolgersi a un consulente abilitato.

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Category Reports Biotech

Tickers reports and analysis

NRx Pharmaceuticals ( $NRXP ) After FY2025: A Multi-Asset Story with Regulatory, Commercial, and Strategic Upside

EN IT Merlintrader Deep Dive | NRXP NRx Pharmaceuticals After FY2025: A Multi-Asset Story with Regulatory, Commercial, and Strategic Upside NRx is no longer just a one-line speculative ketamine story. After the March 2026 annual report and earnings call, the…

Rezolute ( $RZLT ) after the FDA meeting: the congenital HI story is not dead, but the bar is still high

Rezolute remains a classic high-volatility rare-disease biotech story, but the shape of the binary has changed. After sunRIZE missed its primary endpoint in December 2025, many traders effectively treated congenital hyperinsulinism as broken. The March 2026 FDA update forces a more careful read. The agency did not endorse management’s interpretation, yet it also did not dismiss the program outright. Instead, FDA encouraged the submission of comprehensive reports from sunRIZE and the ongoing open-label extension, together with the relevant analysis datasets, for independent evaluation.

ADMA Biologics, Culper Research, and the revenue quality debate ( $ADMA ) (UPDATED march 27 2026 ADMA Fires Back at Culper)

On March 24, 2026, Culper Research disclosed a short position in ADMA Biologics and published a report arguing that the company’s growth story would be overstated by what it described as a channel stuffing scheme involving rebates, extended payment terms, inventory loading, and an undisclosed related-party distributor. Public summaries of the report say Culper’s central claim is stark: absent the alleged sell-in distortion, ADMA’s 2025 revenue would have declined rather than grown. That was enough to break the prior narrative around ADMA as a premium commercial plasma story with unusually strong operating leverage.

Sangamo Therapeutics ( $SGMO ) – Fabry BLA, delivery platform and dilution risk

NASDAQ: SGMO · Biotech · Genomic Medicine · Fabry / CNS Delivery Sangamo Therapeutics (SGMO) – Fabry BLA, delivery platform and dilution risk Biotech report – focus on ST-920 in Fabry disease, Lilly partnership, capital structure and 2026 scenarios. Report…

ImmunityBio’s FDA warning letter is serious — but the market now has to separate management risk from the medicine itself. ( $IBRX )

EN IT Chart source: Finviz. Referral applies only on click. IBRX • Warning Letter • Regulatory Credibility ImmunityBio’s FDA warning letter is serious — but the market now has to separate management risk from the medicine itself ImmunityBio’s sharp March…

Ocugen Inc ( $OCGN ) after the OCU410 12-month readout: alive, arguable, and still risky

There is a lazy way to write this story and a careful way to write it. The lazy way is to say OCU410 either crushed expectations or disappointed the market. The careful way is to admit that the March 24 readout leaves enough evidence for both sides to keep arguing. Ocugen reported that the medium dose chosen for Phase 3 showed a 31% reduction in geographic atrophy lesion growth versus control at 12 months with statistical significance, a 27% slower decline in ellipsoid zone integrity, and no OCU410-related serious adverse events or adverse events of special interest reported to date. That is enough to keep the program alive, credible, and worthy of ongoing attention. It is not enough to eliminate all doubt.

IDEAYA Biosciences ($IDYA): darovasertib timing shift, OptimUM-02 setup, and a full pre-readout deep dive

IDEAYA is one of the more interesting oncology small/mid-cap stories going into spring 2026 because the company sits at the intersection of three things the market tends to pay up for: a registrational catalyst, a platform narrative that is broader than a single-asset biotech, and a balance sheet that is unusually strong for a company still in the clinical stage. The key near-term question is not whether IDEAYA has science or ambition. It does. The real question is narrower and more practical: can darovasertib plus crizotinib in first-line HLA-A2-negative metastatic uveal melanoma deliver a result in OptimUM-02 that is clean enough, strong enough, and regulatorily usable enough to support a credible accelerated-approval path in the United States?

Omeros Corporation ( $OMER ) YARTEMLEA launch, balance-sheet reset, and the real execution test

Omeros is no longer primarily a regulatory story. That phase changed materially on December 23, 2025, when the FDA approved YARTEMLEA for hematopoietic stem cell transplant-associated thrombotic microangiopathy in adults and pediatric patients aged two and older. From that point forward, the central question stopped being “can they get this approved?” and became “can they turn a highly specialized approval into durable commercial traction inside a very concentrated transplant market?”

Weekly recap and next-week setup March 23–27

The week that just ended was not simply another down week for U.S. equities. It was a week in which the market became more severe, more selective and much less willing to pay for fragile narratives. The S&P 500 closed Friday at 6,506.48, the Dow at 45,577.47, the Nasdaq at 21,647.61 and the Russell 2000 at 2,438.45, extending the losing streak for the major U.S. indexes to a fourth consecutive week. The Russell 2000 is now in correction territory from its January high, which matters because it says the weakness is not just about a few mega-cap wobbles. The market is repricing risk appetite more broadly, especially for smaller and more rate-sensitive equities

Travere Therapeutics ( $TVTX ) pre-catalyst deep dive PDUFA APR 13 2026

TVTX is not the typical pre-PDUFA biotech where everything depends on one unproven idea and the balance sheet is already screaming for a financing. Travere enters the April 13, 2026 decision with a drug already commercial in the United States, a meaningful revenue base, a still-usable cash position, and a management team that has already taken FILSPARI from accelerated approval to full approval in IgA nephropathy. That matters. It changes the quality of the setup. It means the market is not being asked to price pure hope. It is being asked to decide how much additional franchise value belongs to FILSPARI if the FDA agrees that the FSGS package is strong enough for approval.

Milestone Pharmaceuticals ( $MIST ) after CARDAMYST approval: from binary FDA story to commercial execution test

Milestone Pharmaceuticals is no longer the same equity story it was in the second half of 2025. For months, the stock traded primarily as a regulatory event setup tied to the resubmitted U.S. application for etripamil in paroxysmal supraventricular tachycardia, or PSVT. That phase ended on December 12, 2025, when the FDA approved CARDAMYST, the company’s first commercial product, as a self-administered nasal spray for the conversion of acute symptomatic episodes of PSVT to sinus rhythm in adults. Since that moment, the question has changed completely. The market is no longer asking whether Milestone can get approved. It is asking whether Milestone can launch, obtain access, build prescription momentum, sustain funding discipline, and then extend the same franchise into atrial fibrillation with rapid ventricular rate, or AFib-RVR.

BioCryst after the transition ( $BCRX ) DD march 20 2026

English Italiano RARE DISEASES · HAE · EARNINGS · FRANCHISE EXPANSION BioCryst after the transition: why BCRX is no longer just an ORLADEYO story, and why the next leg depends on execution BioCryst is not the same company the market…

SELLAS ( $SLS ): March 19 2026 . No longer just a one-shot REGAL trade, but still a high-risk biotech story that has to earn its rerating

SELLAS enters 2026 in a stronger position than it did only a few months ago. The company now has a better-funded balance sheet, a pivotal Phase 3 program that remains the center of gravity for the story, and a second clinical asset that is beginning to matter in a more serious way. That does not make the risk disappear. It simply means the equity story is richer, more credible and more demanding than before.

Fulcrum Therapeutics Inc ( $FULC ) DD March 19 2026

FULC trades on NASDAQ. The stock has benefited from positive Phase 1b PIONEER data announced in late February 2026, which showed robust HbF induction at the 20 mg dose. Current valuation reflects pre-commercialization risk and the clinical timeline for the registration-enabling trial expected in H2 2026.

Cardiff Oncology ( $CRDF ) new AACR breast-cancer angle

Cardiff Oncology has a fresh scientific talking point after announcing preclinical AACR 2026 data around onvansertib in therapy-resistant HER2-low breast cancer models. That headline matters because it expands the mechanistic narrative around the asset. But it does not change the center of gravity of the story. The main valuation engine is still onvansertib in first-line RAS-mutated metastatic colorectal cancer, the company’s cash runway into 2027, and management’s ability to rebuild credibility after the January leadership shock.

Spectral AI ( $MDAI ): DeepView, BARDA backing, FDA De Novo path,

Spectral AI is one of those very small companies where the story looks simple on the surface and much more complicated once you open the hood. The company is trying to bring its DeepView burn-imaging platform through the FDA while using non-dilutive government support to fund part of the journey. The setup is interesting because it combines a real clinical problem, a potentially differentiated imaging workflow, and a government countermeasure angle. The catch is that this is still a micro-cap name with execution risk, regulatory risk, and financing risk that cannot be ignored.

ProKidney (PROK) after FY 2025 earnings

ProKidney’s FY 2025 release did not deliver a dramatic twist, and that is exactly why it matters. Investors were not looking for revenue, because there is none. They were not looking for normal operating leverage, because this is still a pre-commercial biotech. What they needed to see was whether the company could still credibly defend the bridge from today’s balance sheet to the one milestone that truly matters, the Q2 2027 Phase 3 eGFR-slope readout in PROACT 1. For now, the answer remains yes.

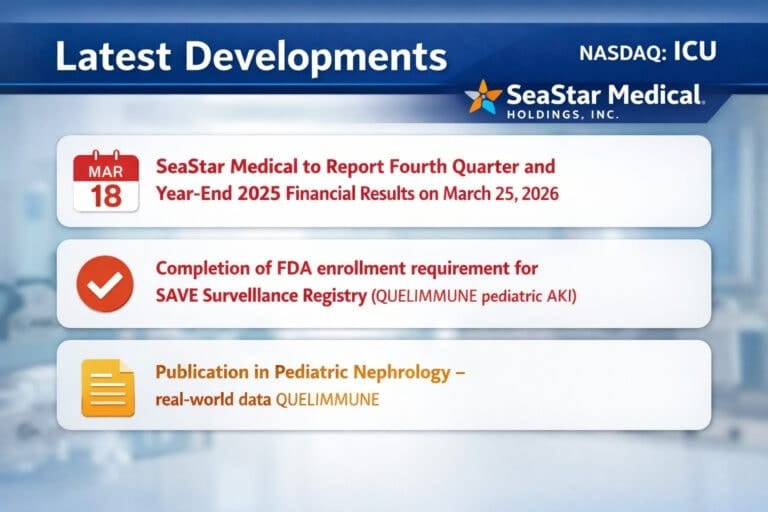

SeaStar Medical ( $ICU ) before FY2025 earnings

SeaStar Medical goes into its March 25, 2026 earnings date with a story that is more credible medically than it was a few months ago, but not yet more comfortable financially. That distinction matters. In ultra-small medtech and biotech names, better clinical framing can improve perception, but it does not automatically repair a pressured capital structure. SeaStar’s recent updates created a more solid pediatric narrative around QUELIMMUNE, yet the company still faces the far more difficult question of whether that narrative can become durable adoption, durable funding and a less fragile 2026 outlook.

Geron ( $GERN ) after FY2025 earnings: RYTELO growth is real, but 2026 now becomes an execution year

Geron’s latest earnings did not kill the bullish case and did not fully validate it either. What they did was more useful: they forced the story into a more serious phase, where commercial consistency, spending discipline and the coming IMpactMF readout matter more than launch excitement.

Protalix BioTherapeutics (PLX) reported fiscal 2025 results on March 18 2026

Protalix BioTherapeutics (PLX) reported fiscal 2025 results on March 18, 2026, with $51.8 million in revenues from selling goods, $52.7 million in total revenues, and a net loss of $6.6 million. The most important near-term development was not just the annual print itself, but the combination of that print with the European Commission approval of the every-four-weeks dosing regimen for Elfabrio, which triggered a $25 million milestone payment from Chiesi.