DISCLAIMER — Not financial advice. Educational content only, not an offer or solicitation to buy or sell any security. Biotech and small/mid-cap stocks are highly speculative and volatile and can result in a partial or total loss of capital. Do your own research and consult a licensed advisor where appropriate. / Contenuti a solo scopo informativo e didattico, non costituiscono consulenza finanziaria né offerta o sollecitazione al pubblico risparmio ai sensi delle normative CONSOB e SEC. Le azioni biotech e le small/mid cap sono strumenti altamente speculativi e volatili e possono comportare la perdita parziale o totale del capitale investito. Si raccomanda di effettuare sempre le proprie ricerche e, se necessario, di rivolgersi a un consulente abilitato.

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Category Reports Biotech

Tickers reports and analysis

Cingulate (NASDAQ: $CING): first full deep dive into the May 31, 2026 FDA binary

Cingulate is one of those micro-cap biotech stories where the entire equity case has compressed into a narrow window: one lead ADHD asset, one PDUFA date, a visible commercialization build-out, and a very real dilution overhang.

Wall Street weekly recap and next-week setup: why April 6–10 became the market’s strongest week since November

A broad and detailed market recap of the week just ended, plus a forward-looking framework for the next one, with focus on inflation spillover, oil structure, U.S.-Iran diplomacy, bank earnings, producer prices and the increasingly important gap between a stabilizing tape and a still-strained real economy.

Celldex Therapeutics (CLDX): the full April 2026 deep dive on barzolvolimab, pipeline breadth, financing, competition and what still has to go right

This is our first full Merlintrader deep dive on CLDX. The core of the story is simple: Celldex is being valued primarily as a barzolvolimab company, but the real debate is whether barzolvolimab can move from an unusually strong phase 2 setup into a durable commercial immunology franchise across CSU, inducible urticarias and potentially additional inflammatory skin diseases.

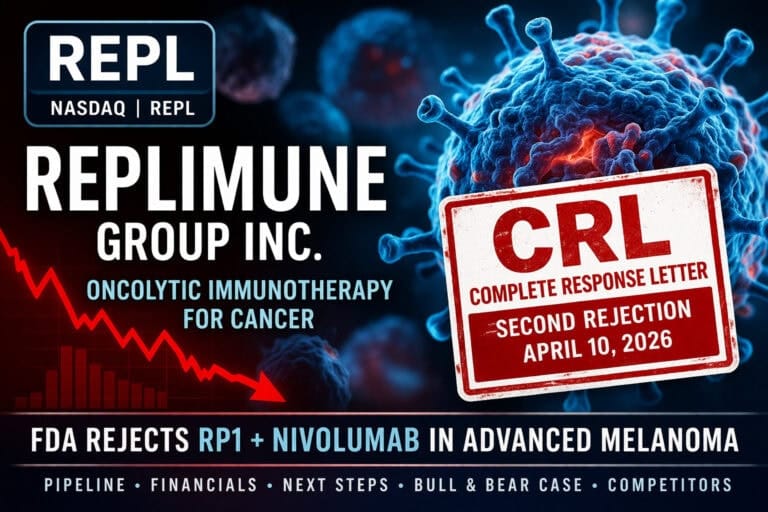

Replimune after the second CRL: why RP1 was stopped again, what still stands, and where the IOVA comparison truly fits

The FDA’s second no on RP1 plus nivolumab in advanced melanoma does not look like a simple administrative delay. It is a rejection that hits the core regulatory thesis, reopens the debate around the program’s near-term value and forces a broader reassessment of the Replimune story as a strategic reset rather than a delayed approval thesis.

Vera Therapeutics (VERA): April 2026 Deep Dive

Vera has moved from a pure data story into a real pre-commercial FDA story. The old thesis was about whether atacicept could produce strong enough renal data to justify a major rerating. The April 2026 thesis is narrower and more demanding: can Vera convert strong upstream biology, a clean Phase 3 interim package and a differentiated at-home profile into approval, a credible first launch, and a durable place in an IgAN market that is no longer empty?

Verrica Pharmaceuticals (VRCA): deep dive 2026 after the balance-sheet reset, the YCANTH ramp and the renewed VP-315 scientific story

VRCA is no longer a simple one-product dermatology story. The company now combines a real commercial base in YCANTH, a large common-warts expansion opportunity with unusually helpful cost-sharing economics, and a basal cell carcinoma asset in VP-315 that continues to add regulatory and scientific credibility. The stock still carries the usual small-cap biotech risks, but the narrative is broader and more interesting than the older “just molluscum and financing stress” version.

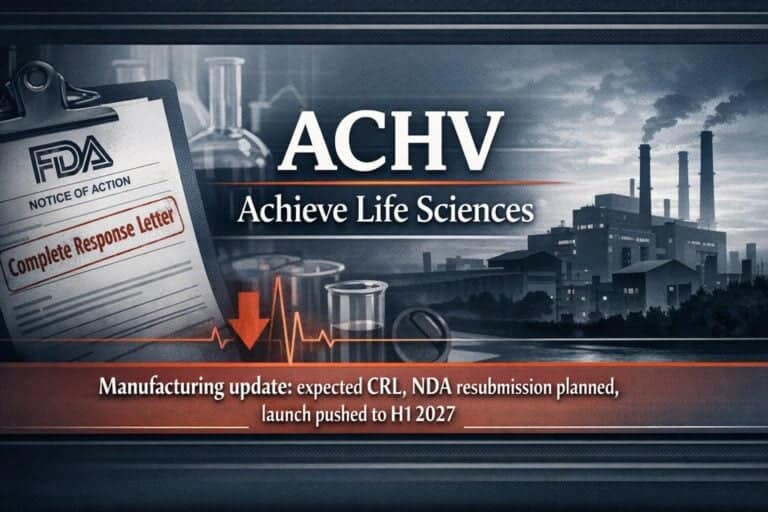

Achieve Life Sciences ( $ACHV) — full April 2026 deep dive UPDATED APRIL 15

ACHV is no longer just a development-stage nicotine-dependence story. It is now a very specific FDA review, launch-prep, manufacturing-readiness and balance-sheet story centered on cytisinicline, with a June 20, 2026 PDUFA date and a second optionality leg in vaping cessation.

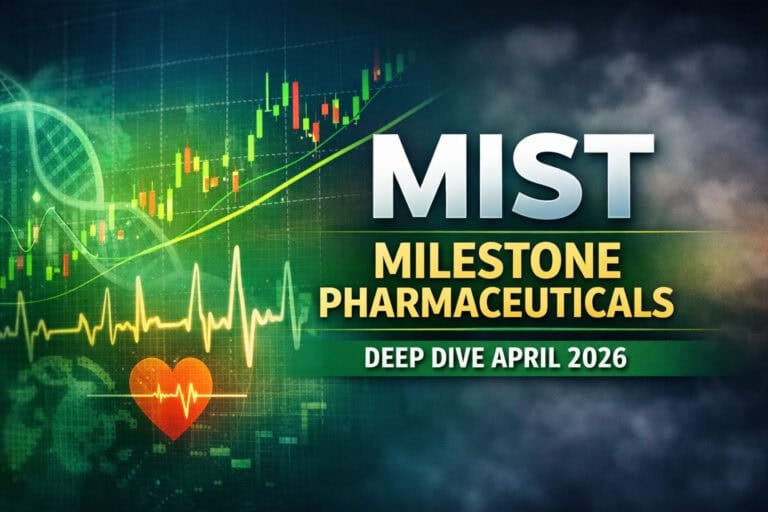

Milestone Pharmaceuticals ( $MIST ) — from approval to execution

The key change since the December 2025 approval is simple: the stock is no longer being judged mainly on whether CARDAMYST can reach the market, but on whether Milestone can actually turn that approval into real access, real prescriptions, real repeat physician behavior, and eventually a broader etripamil franchise beyond PSVT. That sounds less dramatic than a PDUFA setup, but it is usually the more important phase. Approval can rerate a story for a week. Commercial traction is what can rerate it for much longer.

ImmunityBio (IBRX): from the FDA advertising warning to the company’s fix plan, lawsuit noise, and stronger early Q1 revenue

This update picks up the story where the earlier Merlintrader pieces left it: global expansion, label-expansion ambition and clinical momentum were still moving forward, but the market narrative suddenly shifted when the FDA’s Office of Prescription Drug Promotion publicly challenged how ANKTIVA had been promoted. The key question now is not whether the issue existed — it did — but whether the company’s remediation plan is enough to contain the damage while the underlying commercial story keeps improving.

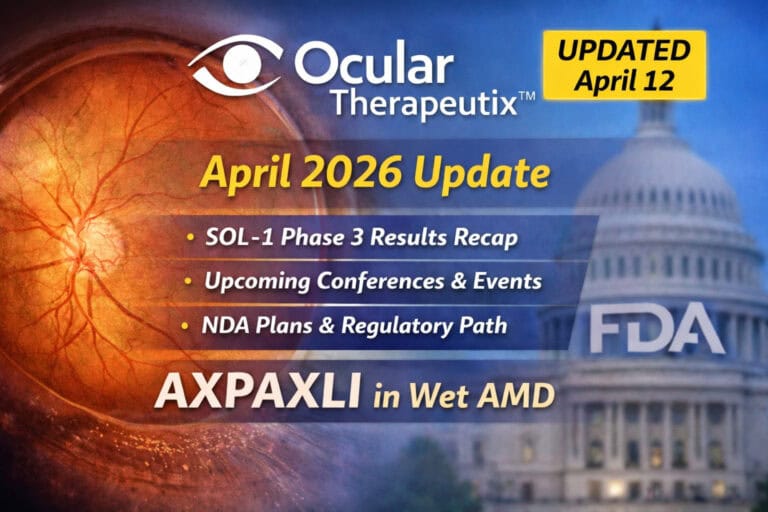

Ocular Therapeutix (OCUL) in April 2026 (Updated april 14)

This April update picks up the OCUL story where our earlier Merlintrader pieces left it: from the pre-readout run-up and takeover chatter, through the February SOL-1 topline and the violent sell-the-news reaction, to the next regulatory, scientific and commercial steps that now matter most.

PMGC Holdings (NASDAQ: $ELAB) — update deep dive April 2026

ELAB is no longer just a tiny “obesity + AI + low float” story. Since the prior Merlintrader article, the company has added another manufacturing asset, widened the NorthStrive pipeline, opened a new defense-tech lane, and fully tapped a $20 million Streeterville facility. That gives it more operational breadth, but it also hardens the core problem: cash is less immediate, dilution is more real, and execution now has to work across biotech, industrial integration and defense optionality at the same time.

Cue Biopharma ( $CUE ) — updated deep dive after the CUE-401 push, CEO transition, and fresh Boehringer milestone

Cue Biopharma is trying to turn a once messy, multi-angle small-cap biotech story into a more focused autoimmune thesis. The company now has a clearer lead asset in CUE-401, a meaningful external validation point through CUE-501 and Boehringer Ingelheim, a recent CEO transition, and a balance sheet that is improved versus the most stressed phase of 2025 but still fragile enough that financing risk cannot be pushed into the background.

Lexicon Pharmaceuticals ( $LXRX ): can Zynquista come back?

A full bilingual deep dive built around the real moving parts of the Lexicon story in April 2026: the Zynquista resubmission path after the 2024 complete response letter, the mid-2026 enrollment target for SONATA-HCM, the cash and dilution picture after the January-February 2026 financing, the economics of the Novo Nordisk LX9851 deal, and the structural risks that still make this name a high-volatility small-cap biotech setup.

Adagio Medical Holdings( $ADGM ) Deep Dive April 2026

Adagio Medical is a very small-cap, pre-commercial medtech name trying to carve out a meaningful niche in ventricular tachycardia ablation with its proprietary ultra-low temperature cryoablation platform. What makes the story relevant now is not revenue momentum, because there really is not much of that yet, but the combination of a pivotal study that has already completed enrollment, encouraging acute data, and a fresh FDA IDE expansion that lets the company clinically evaluate its next-generation ventricular catheter while the broader regulatory path remains open.

Outlook Therapeutics ( $OTLK ) after the new FDA dispute-resolution meeting. What this April review is.

After three Complete Response Letters and a long fight over what counts as sufficient evidence for ONS-5010 / LYTENAVA in wet AMD, Outlook Therapeutics has now moved into a formal FDA dispute-resolution process. This article walks through the CRL history, the new April 2026 meeting, and the real powers of the FDA deciding official — without hype, but also without pretending the door is already shut.

CorMedix ($CRMD): the real second chapter after commercialization

DefenCath is no longer just a launch story, and CorMedix is no longer easy to reduce to a one-drug binary. The company now has real revenue, positive adjusted EBITDA, a broader anti-infective platform after the Melinta transaction, and an approaching Phase 3 readout for REZZAYO. But it also has one very specific pressure point that still dominates the equity story: the July 1, 2026 reimbursement transition for DefenCath. This report is built to cover every major angle ahead of the ReSPECT topline update and to explain, from first principles, why the reimbursement framework matters so much.

REPL, TVTX, GRCE: three April 2026 PDUFA decisions that matter

A full editorial deep dive on the three most interesting April biotech FDA setups still ahead: Replimune, Travere Therapeutics and Grace Therapeutics. Each story carries a different kind of risk. Replimune is the credibility test after a prior CRL. Travere is the commercial expansion test for a product that already sells. Grace is the classic small-cap binary setup where one approval could change the company’s profile very quickly.

Atea Pharmaceuticals ( $AVIR ) Deep Dive

Atea Pharmaceuticals is now best understood as a concentrated, late-stage antiviral bet built around a single core opportunity: the fixed-dose combination of bemnifosbuvir and ruzasvir for chronic hepatitis C. The company is not being valued today for a sprawling platform with multiple near-term revenue paths. It is being judged mainly on whether its HCV regimen can validate in Phase 3, differentiate clinically and commercially, and then support a credible regulatory path into 2027.

Viridian Therapeutics (VRDN): after the crash, what still matters now?

Why this follow-up exists

REVEAL-1 did not kill the TED thesis, but it changed the bar. The debate has moved from “does the drug work?” to “can Viridian still build a differentiated TED franchise that deserves premium valuation?”

Wall Street weekly recap and next-week setup: why March 30–April 3 became a relief week

Executive summary

The week that ended on Friday, April 3, was not a clean return to bullish calm. It was a relief week inside an unresolved macro problem. U.S. markets were closed on Good Friday, so the real trading week ended on Thursday, April 2. By then, the S&P 500 had posted a weekly gain and broken its five-week losing streak, while Wall Street had spent the entire week bouncing between fear of an extended energy shock and hope that the war-driven disruption around Iran and the Strait of Hormuz might not become a permanent economic wound.