DISCLAIMER — Not financial advice. Educational content only, not an offer or solicitation to buy or sell any security. Biotech and small/mid-cap stocks are highly speculative and volatile and can result in a partial or total loss of capital. Do your own research and consult a licensed advisor where appropriate. / Contenuti a solo scopo informativo e didattico, non costituiscono consulenza finanziaria né offerta o sollecitazione al pubblico risparmio ai sensi delle normative CONSOB e SEC. Le azioni biotech e le small/mid cap sono strumenti altamente speculativi e volatili e possono comportare la perdita parziale o totale del capitale investito. Si raccomanda di effettuare sempre le proprie ricerche e, se necessario, di rivolgersi a un consulente abilitato.

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Red Cat Holdings ($RCAT) — a full 2026 deep dive after earnings, Apium, Ukraine and the new NATO order

Red Cat is trying to move from being treated like a single-product drone story into a broader autonomy and defense platform. The company has given the market a dense sequence of catalysts in less than three weeks. The real question now is not whether the story sounds better. It clearly does. The real question is whether that upgraded story can hold up once investors start demanding harder commercial evidence.

Viridian Therapeutics (VRDN): after the crash, what still matters now?

Why this follow-up exists

REVEAL-1 did not kill the TED thesis, but it changed the bar. The debate has moved from “does the drug work?” to “can Viridian still build a differentiated TED franchise that deserves premium valuation?”

Wall Street weekly recap and next-week setup: why March 30–April 3 became a relief week

Executive summary

The week that ended on Friday, April 3, was not a clean return to bullish calm. It was a relief week inside an unresolved macro problem. U.S. markets were closed on Good Friday, so the real trading week ended on Thursday, April 2. By then, the S&P 500 had posted a weekly gain and broken its five-week losing streak, while Wall Street had spent the entire week bouncing between fear of an extended energy shock and hope that the war-driven disruption around Iran and the Strait of Hormuz might not become a permanent economic wound.

Cannabis policy 2026: what Schedule III could really change

The most interesting part of the current cannabis setup is not a headline or a price spike. It is the possibility that the United States is slowly moving from a regime of blanket federal hostility to one of selective federal accommodation. That would be a major change. It would not, however, be the same thing as a clean legalization story.

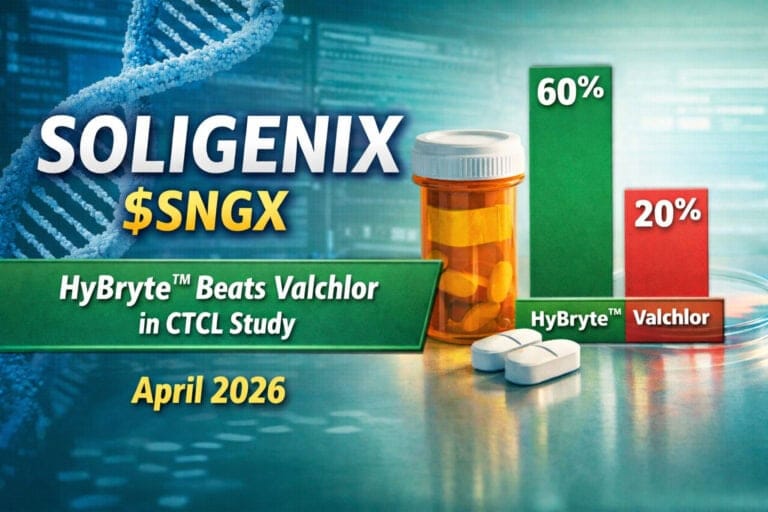

Soligenix ( $SNGX ): HyBryte vs. Valchlor, the full story from the first comparison to today

Soligenix is a micro-cap biotech whose current equity story lives or dies largely on the fate of HyBryte in early-stage cutaneous T-cell lymphoma. The April 2, 2026 press release is real and meaningful, but not because it introduces the HyBryte-versus-Valchlor numbers for the first time. Those numbers were already disclosed in 2024. What is genuinely new is that the dataset has now been republished and reframed in a scientific setting, giving more external legitimacy to the claim that HyBryte may be clinically differentiated.

Lipocine ($LPCN) — after the 78% collapse: what is left, what broke, and what management can realistically do now

Lipocine entered April 2 as a micro-cap biotech still largely defined by one late-stage binary event. It exits the day as a radically repriced company. The reason is simple: LPCN 1154 failed its Phase 3 primary endpoint in postpartum depression. In the full study population of 90 patients, the company said the drug did not show a statistically significant reduction versus placebo in HAM-D17 at hour 60. That single fact destroyed the old near-term bull case and triggered a collapse of roughly 78% in the stock. What the market is doing is not subtle. It is saying that the company’s main value-driving asset just lost most of its immediate strategic and regulatory premium.

Ballard Power Systems: from hydrogen hype to operational turnaround – execution matters now

Ballard Power Systems entered 2026 after one of the clearest operational resets seen across listed hydrogen names. After a painful 2024, when revenue fell 45% and the company announced a major restructuring, FY 2025 brought a real reversal in the numbers: revenue of $99.4 million, up 43% year over year, nearly 800 fuel cell engines delivered and more than 75 megawatts shipped, and gross margin of 5% for the full year, compared with deeply negative levels in 2024. Most importantly, Q4 2025 generated $11.4 million of cash flow from operating activities, while full-year cash usage fell by 50% versus 2024.

AbCellera Biologics ( $ABCL ) — deep dive on platform, pipeline, cash, insiders, institutions, and the road ahead

There is an old way to describe AbCellera and a newer, more accurate way. The old way is to call it a technology platform for antibody discovery that collaborates with larger pharmaceutical companies and occasionally captures royalties or milestone economics downstream. That is still partly true, but it no longer captures the real center of gravity. The company says explicitly that it has evolved from using the platform primarily for partner programs toward building its own internal pipeline of AbCellera-owned assets, and by 2025 that strategic transition had effectively reached the clinic.

Redwire QKDSat – European Quantum Security and the Broader 2026 Narrative

Redwire’s 2 April 2026 QKDSat announcement matters less for immediate revenue math and more for what it says about the company’s position inside the next layer of European sovereign space infrastructure.

According to publicly reported company news on 2 April 2026, Redwire was awarded a contract connected to the European Space Agency’s Quantum Key Distribution Satellite (QKDSat) program. The mission is framed around a quantum-secure spacecraft and sits within the broader ESA ARTES ecosystem, which is designed to support advanced telecommunications and secure connectivity programs.

Foundayo gets there first, and it is a pill: why this approval really changes the competitive setup for Altimmune and Viking

The FDA approval of Foundayo, Eli Lilly’s oral small-molecule GLP-1, does not automatically destroy the cases for Altimmune or Viking Therapeutics. But it does make the field more selective and far less forgiving. Lilly is not just early. Lilly is early with an approved product, near-term availability, an already powerful weight-management brand, a pill format that lowers the psychological barrier to starting therapy, and a commercial message built around access and simplicity. From this point forward, it is no longer enough to say that an obesity candidate has promising data. The real question is why the market should wait for it when the category leader has already put a real pill, ready for launch and ready for normalization inside the treatment pathway, on the table.

Eli Lilly ( $LLY ) — Foundayo’s FDA approval may be more than a product launch

The FDA approval of Foundayo, the brand name for oral small-molecule GLP-1 orforglipron, matters well beyond the usual “new drug approved” headline. Lilly already had one of the most powerful obesity franchises in the world through Zepbound. What it lacked was a simpler oral front door into the same therapeutic universe. Foundayo changes that. It adds a once-daily pill, no food restrictions, no water restrictions and an immediate commercial launch path. More importantly, it gives Lilly a second format that could widen the patient funnel, reduce psychological barriers to treatment initiation and deepen control over the obesity journey from entry-level adoption to higher-intensity therapy.

Artemis II — A Tribute to the Brave Who Walk Toward the Future

Apollo was one of the defining achievements of the twentieth century, but it also left behind a strange inheritance. It proved that human beings could leave Earth, navigate across cislunar space, land on another world, and come home. Then, after proving it, the United States stopped going. The Moon remained in the cultural imagination, in schoolbooks, documentaries, museum halls, and old family conversations, but not in the rhythm of ordinary current events.

Firefly Aerospace ( $FLY ) Alpha Flight 7 worked

Firefly is easier to understand after March 2026 than it was a few months ago. Alpha Flight 7 reached orbit, delivered a Lockheed Martin payload, performed a stage-two relight, and validated key Block II upgrades ahead of Flight 8. That matters because the company badly needed a clean operational proof point after prior launch and test setbacks. The core story today is no longer “can Firefly do anything?” but “can Firefly string multiple wins together without burning too much cash along the way?”

Tilray Brands ( $TLRY ): Q3 FY2026 says the story is still alive

In early March, the core question around Tilray was not whether the company could tell a big story. It was whether that story was finally becoming tangible. Q3 FY2026 does not solve every doubt, but it does move the debate forward: cannabis improved, distribution stayed strong, margins held up better than feared, adjusted EBITDA grew, and the balance sheet still looks workable. The weak point remains the same one the market keeps circling around: beverage execution and the long shadow of dilution.

Sidus Space ( $SIDU )after Q4 2025: our thesis, what is being confirmed, and what still needs to be proven

Sidus Space has become one of those names that attract attention for a reason. It sits at the intersection of several powerful themes — small satellites, on-orbit processing, dual-use space and defense technology, edge AI, and the broader U.S. national-security buildout. But attractive themes alone are not enough. The real question for investors has always been simpler and harder at the same time: is Sidus merely assembling a compelling narrative, or is it actually building a business that can one day justify the story?

Omeros ( $OMER ): the post-approval story is finally turning, early commercial momentum is here, and the next upside chapter may be starting

The new March 31, 2026 press release did not simply deliver an earnings update. It effectively marked the first real post-approval checkpoint for Omeros. The company is no longer only a regulatory event story. After the December 23, 2025 FDA approval of YARTEMLEA for TA-TMA and the January 2026 U.S. launch, the central question has changed. The market is now asking whether the company can convert medical need, regulatory exclusivity and first-mover status into a durable commercial franchise.

Aquestive Therapeutics After the CRL ( $AQST ): what changed, what still matters, and how much balance-sheet room is left

Where the story stands today is more nuanced than the tape action around the January disappointment made it look. The FDA did not throw out the Anaphylm package because the drug failed on efficacy, because the core clinical bridge broke, or because major chemistry, manufacturing, and controls issues surfaced. The company’s February disclosure said the Complete Response Letter was focused on administration, labeling guidance, human factors deficiencies, and one supportive pharmacokinetic study tied to the packaging and labeling changes. In plain English, this was bad news, but it was not the same thing as a fundamental collapse of the program.

The market then needed a second question answered: would management actually get the FDA onto a defined remediation path, or would this turn into a vague, open-ended delay? The March 30 Type A meeting update is important because it is the first sign that the post-CRL process is becoming more concrete. AQST said the FDA gave clarifying feedback on both the PK and human factors study designs, acknowledged the changes to the pouch opening mechanism, and aligned on the concept of using labeling language to manage potential chewing of the film rather than demanding additional clinical data. That does not mean approval is in the bag. It does mean the company has moved from uncertainty to a more actionable playbook.

Axsome Therapeutics ( $AXSM ) — March 31, 2026 deep dive: setup to the April 30 PDUFA

A full follow-up report built from the January 2, 2026 setup and updated through March 31, 2026, focused on the Alzheimer’s disease agitation PDUFA, commercial momentum, management depth, cash and dilution risk, ownership, sell-side posture, retail sentiment, forward catalysts, scenarios, red flags and bottom line.

Polar Power Inc ( $POLA )

Polar Power, Inc. (NASDAQ: POLA) is a Gardena, California-based designer and manufacturer of direct current (DC) power generation systems serving telecommunications, military, commercial, and industrial markets globally.

As of the quarter ended September 30, 2025 and filed on November 19, 2025, POLA was in severe financial distress. Primary-source review confirms $4K cash, sharp year-over-year sales deterioration in Q3 2025, and material pressure on liquidity and financing. The original draft referenced a going concern warning from auditors, an eviction summons on the headquarters facility, lender covenant breach, and a $5.3M backlog. Of these, the cash position and broader distress are confirmed directly by the 10-Q; some of the more specific legal and audit formulations require direct supporting passages beyond what was fully retrieved in this review.

This remains a binary turnaround speculation, not an investment-grade opportunity. Execution on backlog, continued lender tolerance, and facility continuity could support survival. Failure on one or more of those fronts would materially increase restructuring or bankruptcy risk.

Agios Pharmaceuticals ( $AGIO ): the story did not end with the sickle-cell disappointment

Agios is not the same story it was one year ago, and it is not even the same story it was right after the market reacted badly to the November 2025 RISE UP data. The cleanest way to frame the company today is not as a single-product binary biotech and not as a fully de-risked rare-disease compounder either. It sits somewhere in the middle. There is now a real commercial base, a very strong balance sheet by biotech standards, a broader geographic footprint for mitapivat in thalassemia, and a reopened regulatory path in sickle cell disease that most investors had at least partially discounted after the mixed Phase 3 readout.